Powering the AI Revolution: Rethinking the Future of US Data Centres

Despite America's dominance, a perfect storm of constraints threatens to reshape the global data centre landscape, with Latin America emerging as a formidable competitor.

This article was originally written by Yellow Radio for Fluix.ai and published here.

The data centre industry is at an inflection point. Despite America’s current dominance, a perfect storm of constraints threatens to upend the established order, particularly as Latin America emerges as a formidable competitor in the global AI infrastructure landscape.

The Paradox of American Dominance

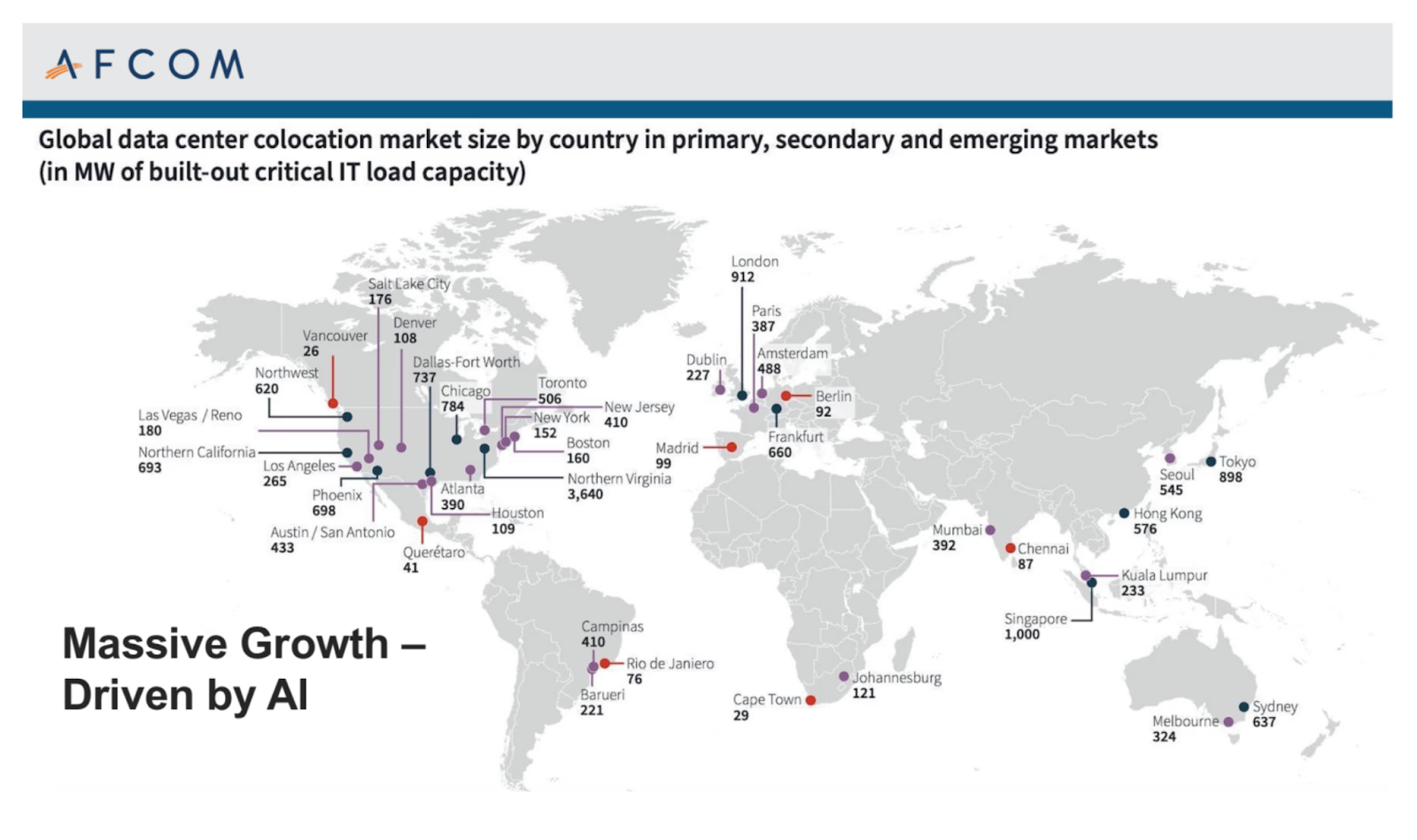

It’s difficult to imagine the US relinquishing its data centre supremacy. With over 5,000 facilities across the mainland and a market valued at approximately $100 billion in 2024 (projected to reach $150 billion by 2030), America’s infrastructure dwarfs the rest of the world by a factor of 10 according to industry analyses. The concentration of AI innovation companies on US soil further reinforces this apparent advantage.

Yet this dominance masks critical vulnerabilities when examined through seven key perspectives that truly determine competitive advantage in this space.

A Tale of Two Continents: LatAm’s Rising Challenge

Having recently attended both Data Center World (DCW) in Washington DC and Capacity LatAm in São Paulo, the contrast between North and Latin American approaches is striking. While the US struggles with increasingly complex constraints, Latin America is rapidly evolving its capabilities and cultivating new market relationships.

The LatAm data centre market, valued at $7.16 billion in 2024 and projected to reach $14.3 billion by 2030 (12.2% CAGR), represents a fraction of US capacity today according to recent market research. However, its growth trajectory and structural advantages demand serious attention. Brazil, Mexico, Chile, and Colombia led market investments in 2024 and are expected to continue their leadership position.

The Seven Critical Factors Reshaping the Competitive Landscape

1. Land: Scarcity vs. Abundance

In the US, land acquisition remains one of the most critical (and increasingly problematic) factors for data centre development. Major investments like Atlas’s proposed $17 billion development across 832 acres in Georgia and Tract acquiring 2,200 acres in Storey County highlight the scale of land requirements. However, zoning issues and permitting delays create significant barriers to expansion.

Meanwhile, Latin American nations enjoy significant land availability and are actively positioning data centre builds as economic growth drivers. In Brazil alone, Scala has acquired 700 hectares for an AI city in Eldorado do Sul, while Elea announced a $1 billion expansion plan as reported by industry analysts. The region is investing over $2 billion in land acquisition and secondary market development, with fewer regulatory obstacles.

2. Energy: Constraint vs. Opportunity

Energy supply has become one of the primary constraints for US data centre expansion. Many operators, particularly hyperscalers, are now forced to develop local on-site, microgrid, or hybrid solutions to supplement grid capacity. While this drives innovation in energy supply, including gas turbines, Small Modular Reactors (SMRs), and Battery Energy Storage Systems (BESS), the fundamental constraint remains.

Contrast this with many Latin American countries, where energy supply is both resilient and competitively priced: commercial rates as low as $0.03/kWh in Argentina compared to substantially higher costs in most US regions according to industry reports. Government subsidies in oil-rich nations maintain these advantageous rates.

Moreover, renewable energy potential across Uruguay, Paraguay, Costa Rica, Bolivia, and Brazil represents a largely untapped opportunity, currently limited only by internet connectivity infrastructure. These countries have significant renewable energy production capability that could be leveraged for data centre operations once connectivity issues are addressed.

3. Connectivity: Saturation vs. Expansion

US data centres generally enjoy high-capacity, low-latency fiber connectivity for domestic services. However, last-mile contention and saturation increasingly limit consumer bandwidth, reducing the native advantage that US data centres maintain over LatAm facilities serving US customers.

Latin American countries, particularly Brazil, Chile, Mexico, Colombia, and Panama, have heavily invested in submarine cable landing stations and Internet Exchange Points with robust fiber infrastructure. For serving global traffic, geography still matters; Panama may have a measurably lower Round Trip Time (RTT) to Florida than Chile, though the difference is not material for many applications.

4. Water: Scarcity vs. Abundance

Water has become a critical limiting resource in many US regions, forcing the adoption of alternative sources (gray water) for cooling and industrial usage such as fire suppression. Ongoing climate uncertainty only exacerbates this constraint.

By contrast, many Latin American countries enjoy significant rainfall and water reserves. Though unevenly distributed across the continent, water remains a relatively abundant resource for data centre operations (whether for evaporative cooling, energy production, or fire management) throughout much of the region.

5. Cooling: Innovation Through Necessity

Cooling technology remains a constant yet ever-evolving theme at data centre conferences across both continents. Air cooling continues to dominate with 80%+ adoption due to its relative maturity, operational simplicity, and lower cost structure. However, as compute densities increase, more efficient cooling solutions become imperative.

Liquid cooling technologies are gaining traction, with several distinct approaches emerging:

- Direct-to-chip cooling: Brings coolant directly to the processor through plates attached to components, allowing for more targeted heat removal

- Single-phase immersion cooling: Submerges components in a non-conductive liquid that absorbs heat but doesn’t change state

- Two-phase immersion cooling: Uses liquids that vaporize at low temperatures, creating a more efficient cooling cycle through phase changes

Studies have shown that liquid cooling can reduce facility power consumption by up to 27% and improve total facility efficiency by over 15% according to research from NVIDIA and Vertiv. Despite these advantages, implementation remains challenging due to the increased cost, complexity, and operational risks they introduce. A presentation at DCW attributed 4% of GPU errors to liquid cooling leaks.

The adoption of advanced cooling technologies is accelerating faster in the US, driven by necessity, with many operators transitioning to hybrid cooling approaches that combine air and liquid cooling methods to optimise performance.

6. Supply Chain: Vulnerability vs. Opportunity

The current geopolitical landscape creates significant supply chain challenges for both regions. However, their responses differ markedly.

In the US, operators are stockpiling components to hedge against future disruptions and price fluctuations, a defensive strategy that adds cost and complexity. While the general sentiment at DCW was calm and optimistic, concrete actions suggest underlying concern.

Latin America, meanwhile, is actively developing new supplier relationships, particularly with APAC and ASEAN vendors eager to expand their market reach. The region views export restrictions, especially on Nvidia GPU chips which dominate the AI industry, as a short-term challenge and longer-term opportunity for alternative suppliers like Huawei to increase market share and accelerate innovation.

7. Regulation: Obstacle vs. Enabler

Perhaps the most significant contrast lies in regulatory frameworks. US data centres face some of the strictest and slowest regulatory processes globally, particularly regarding land zoning, construction approval, and resource usage authorization. These constraints significantly delay new developments, to the point where some operators reportedly proceed with construction before securing permits, accepting substantial risk to meet market windows.

Latin American regulatory frameworks, while strict, generally offer faster permitting processes for construction and deployment, enabling more rapid market response.

The Unseen Dimensions

What remains largely undiscussed at industry events across both continents are the truly innovative approaches that could reshape the industry: mixed-use developments optimising energy reuse, fundamental shifts in AI service delivery models, potential alternatives to Nvidia’s GPU dominance, and the evolution of frontier models toward AGI capabilities.

The security requirements and risks of co-locating data centres with commercial or residential properties make such optimisations nearly impossible, despite their potential benefits for heat and energy reuse. Similarly, there was little discussion about whether the current dominance of Nvidia in the GPU industry might shift toward new suppliers or approaches, such as synthetic GPUs or alternate architectures.

As events like the emergence of Deepseek demonstrate, long-held assumptions about compute requirements for training and inference workloads may be challenged more rapidly than the industry anticipates. Similarly, the future of frontier models, particularly regarding multi-modal capabilities and AGI (and perhaps one day, ASI), remains largely undebated.

The situation is quite different in the Nordics and APAC/ASEAN regions, particularly regarding variations in energy supply (for example geothermal) and climate conditions that impact cooling efficiency.

What for now remains a safe assumption is that demand will outstrip supply for the next 5 years, with data centre electricity demand in the US projected to more than double from 185 TWh in 2023 to 440 TWh by 2035 according to S&P Global data.

America’s Path Forward

The US continues to lead in data centre capability, particularly for AI service delivery. However, Latin America’s growth trajectory and the establishment of new trading partnerships, particularly through Brazil’s BRICS relationships, suggest a shifting competitive landscape.

For the US to maintain its leadership position, three critical changes are necessary:

- Accelerate, simplify, and optimise regulatory frameworks to enable faster data centre expansion

- Reconnect with America’s core competitive advantage: innovation capacity and creative problem-solving

- Drive improvements in compute density, cooling efficiency, and chip design to increase compute-per-megawatt capabilities

With more holistic, sustainable approaches to renewable energy utilisation and smarter resource management, particularly water, the US can extend its leadership position despite mounting challenges.

Industry Transformation Through Optimisation

As a leading provider of intelligent data centre optimisation solutions, Fluix has demonstrated that significant efficiency gains are achievable through optimised cooling infrastructure and waste elimination. In production environments, Fluix AI autopilot has achieved 40-50% reduction in HVAC energy. Their technology is now being deployed within colocation data centre customers in LatAm and being distributed through major US utility curtailment programs.

This optimisation-focused approach represents America’s most promising path forward: leveraging its innovation capacity to solve complex efficiency challenges rather than simply expanding physical infrastructure.

The global AI race will not be won through brute-force expansion of traditional data centre models. Victory will come through creative reinvention of how we design, build, and operate these critical facilities, balancing resource constraints with performance demands through technological innovation.

The question is whether US data centres will continue to dominate in a world where competitive advantage increasingly flows from efficiency rather than scale.

Got comments?

We'd love to hear your thoughts on this article.

Thanks for your feedback

We appreciate you taking the time to share your thoughts.

Something went wrong. Please try again, or email us directly at contact@yellowrad.io.